Case Study: Luckin Coffee Accounting Fraud

By Emma Chung

The following describes the Luckin Coffee accounting fraud with details of responsible parties, events, and financial misconduct in the case of Securities and Exchange Commission vs Luckin Coffee. This case was settled in December 2020.

PARTIES

The core parties in this case include:

Luckin Coffee Inc. (Luckin)

Luckin is a beverage retailer in China selling mainly coffee and tea. After opening its first Beijing and Shanghai stores in January 2018, Luckin rapidly expanded by establishing 4,507 stores in the following two years. Luckin claimed it served more than 40 million customers as of the end of 2019[1], becoming the largest coffee retailer in China, overshadowing its rival, Starbucks, in the region. In a bid to increase market share, if consumers purchased Luckin products with coupons via the company’s app, Luckin offered them sizeable discounts or free products. Specifically, Luckin provided two methods for consumers to buy goods, either (1) through a digital payment platform operated by a third-party, such as WeChat Pay or Alipay,[2] or (2) by redeeming coupons through Luckin’s app. Customers could buy these coupons in advance through Luckin’s app by transferring money from WeChat Pay or Alipay.[3] According to Luckin, the revenue from the sale of coupons was calculated based on the number of redemptions, instead of the actual number of coupons sold.

The US Securities and Exchange Commission charged Luckin with fabricating untrue statements from April 2019 to January 2020 regarding revenue, expenses, and net loss so as to deceive investors about Luckin’s financial performance.[4] In December 2020, China-based coffee retailer Luckin agreed to pay USD180 million to settle charges of fraud and accounting irregularities.

Securities and Exchange Commission (SEC)

SEC is a federal government regulatory agency that oversees securities markets to ensure accountability, transparency, and fair financial transactions. It aims to protect investors from financial irregularities and monitor the listed company’s actions in the US. The SEC has the authority to bring a civil action against an individual or company and impose civil penalties.

Luckin’s Senior Management

The senior management of Luckin has a fiduciary duty to certify and ensure financial statements are accurate. Former Chairman Charles Zhenyao Lu, former CEO Jenny Zhiya Qian, and former COO Jian Liu failed to maintain the strong internal controls necessary to ensure reliable financial statements and the accuracy of transactions.

Luckin’s Board of Directors

The board of directors are responsible for overseeing Luckin’s management and spotting unethical practices. Luckin’s former COO, Jian Liu, resigned in April 2020, admitting he had overstated the company’s revenue. A number of directors and the chairman were replaced after a general meeting was held in July 2020.

Muddy Waters LLC (Muddy Waters)

Muddy Waters is an investment research firm based in the US. It conducts research about financial fraud. Seven Pillars Institute is of the view that “Muddy Waters’s combination of short selling and equity research is a clever business model, necessary to satisfy the market’s need for research analysts or firms independent of sell-side companies.”[5]

Short-seller Muddy Waters Research received an anonymous report, together with supporting evidence in January 2020, alleging the fraudulent conduct of Luckin.[6] Muddy Waters publicly posted this report to its Twitter account and did not indicate how it obtained the anonymous report.[7]

The report alleged that Luckin fabricated performance through inflated revenue, coupon sales, and redemptions. The report questioned Luckin’s practices and revealed the falsified sales volume. The report showed that Luckin marked up its sales volume by 69% in the third quarter of 2019 and 88% in the fourth quarter of the same year.[8] Further, the report raised questions about the inflated revenue, false accounting practices, and abuse of senior management positions. The report also questioned the extraordinary market share of coffee sales in China that Luckin claimed, given most caffeine intake in China comes from tea, as in most countries in Asia.[9] Muddy Waters said it decided the share price of Luckin would drop and had sold short Luckin’s shares after releasing the report to the public.[10]

(Source: Luckin Coffee[11])

Audit Committee

The audit committee is a board committee of members responsible for monitoring external auditors and making sure the internal controls to prevent false accounting are robust. The members of Luckin’s former audit committees, Tianruo Pu and Sean Shao, resigned from the board in June 2020.[12] In Luckin’s case, the audit committees failed to conduct due diligence and question the fabricated transactions. Instead, the committee delegated its responsibility to management. This raises the question of the extent to which independent directors can freely advise, given they are paid by management. Directors also rely on management to provide accounting information and financial performance data.

Internal Auditors

Internal auditors are responsible for overseeing accounting accuracy and compliance procedures.[13] In Luckin’s case, there was a business operations database that showed the actual transactions of sales, redemptions, and orders.[14]However, another database comprising the fabricated transactions was used to prepare the false financial statements. The financial department only had access to the fabricated database and was unable to verify the accuracy of the transactions. Internal auditors not only failed to spot the abnormal transactions, they also cooperated in fabricating the company’s performance in the financial statements.[15]

External Auditor

Ernst & Young Hua Ming LLP (EY) was the external auditor for Luckin. EY made two public statements about Luckin. The first made in April 2020, stated EY had found the fabricated revenue and expenses from 2019 and reported it to the board. The second statement, made in July 2020, provided further details and stated it recognized irregularities in January 2020 and immediately raised red flags. EY denied any responsibility in the scandal. EY audited Luckin’s 2017 and 2018 financial reports, which were part of the company’s IPO prospectus, but did not audit the 2019 financial statements.[16]However, EY wrote a private letter to a number of investment banks stating it did not have an issue with the financial performance of Luckin in the first three quarters of 2019.[17] This letter was issued before the 2019 financial statements were audited.

EVENTS

IPO Launched

In May 2019, within 18 months of Luckin’s grand opening, the company launched its IPO of American Depositary Shares in the United States and listed on Nasdaq. The first United States listed coffee retailer based in China, Luckin made roughly USD600 million from investors. Operating 2,370 stores in China in March 2019, the company claimed its “disruptive model has fulfilled the large unmet demand for coffee and driven its mass-market consumption in China… allowing us to achieve significant scale and growth”[18]. Luckin also reported its revenue reached USD71.3 million in the first quarter of 2019 – more than half of the total revenue for the whole of 2018. Luckin highlighted its rapid growth in the first quarter of 2019, pointing to quantity of products sold, cumulative consumers, number of stores, and revenue. The company’s estimated market value increased from USD1 million in July 2018 to USD3.9 billion in May 2019. The public report of Luckin‘s rapid growth pushed the value of the company to USD5 billion. The company was delisted from the Nasdaq on 29 June, 2020.

(Source: Luckin’s announcements, Media reports and Caixin[19])

Luckin’s Fabricated Sales

It was later revealed Luckin had been using fabricated coupon sales to inflate its revenue from the beginning of April 2019, with employees being involved in three types of fraudulent schemes. Deals were done by fabricating coupons to three groups of consumers: individual customers, corporate customers, and sales to third-party shell companies – intermediary agents that would resell coupons to individual customers. Indeed, some of Luckin’s management and employees were aware of the schemes and the false accounting.[20]

First Fraudulent Scheme

In April 2019, Luckin began fabricating the number of coupons sold and redeemed by individual customers. Some of Luckin’s employees, their family members, and other related companies transferred money from private bank accounts to their WeChat Pay or Alipay accounts in order to purchase coupons on Luckin’s app.[21] They then redeemed the coupons and created fake orders, thereby intentionally and dishonestly increasing sales figures. More than USD1 million of sales was fabricated in the first scheme. It is uncertain whether Luckin recycled the money back to the employees so they could purchase more coupons. However, Luckin recognized the fabricated revenue.[22]

Second Fraudulent Scheme

In May 2019, Luckin employees began selling coupons to fake corporate customers, who were, in fact, related to Luckin employees. The corporate customers would transfer money from their corporate WeChat Pay or Alipay accounts to Luckin’s app to buy coupons. Similar to the first scheme, these fake coupon redemption orders artificially enhanced sales performance. Roughly USD10 million of sales were fabricated in the second scheme. However, it is uncertain whether Luckin recycled the money back to the employees.

Third Fraudulent Scheme

Beginning in May 2019, the third scheme saw Luckin employees fabricate the number of coupons sold to third-party shell companies. These shell companies would then resell the coupons to individual customers. It is likely these individual customers were also employees as they neither placed real orders nor redeemed the coupons.[23] Some of Luckin’s employees or their related companies established and controlled these shell companies, which transferred funds to Luckin. Employees would then change the name of the sender from the funding company to the shell company in Luckin’s bank statements. Luckin’s employees would redeem coupons and make fake orders, fabricating coupon sales and revenue. This made up the largest portion of fabricated revenue, approximately 90% of the total USD311 million.

Some Luckin employees switched the source data from the actual business operations database to the fabricated database. Source data includes reports necessary for preparing financial statements and bookkeeping. Luckin’s finance department could only access the fabricated database and thus failed to notice the abnormal transactions.

Fabricated Expenses and Returned Funds

Luckin returned funds to the funding companies in the third scheme through bank transfers and fabricated expenditure. Business-related expenses, as set out in the financial statements, showed that there were payments to vendors, including suppliers. However, these vendors did not provide any services or products to Luckin in return. Luckin also fabricated costs so that they were consistent with the overstated revenue. In 2019, the total fabricated expenses and costs were around USD196 million.

(Source: The Wall Street Journal[24])

Earnings in the second quarter of 2019: Luckin substantially overstated its revenue by 27%, expenses by 9%, and net loss was understated by 15%.[25]

Earnings in the third quarter of 2019: Luckin’s revenue and expenses were overstated by 45% and 24%, respectively, and its net loss was understated by 34%. Further, Luckin’s share price increased 60% from the IPO price.[26]

Fabricated sales and expenses in the fourth quarter of 2019: Luckin continuously fabricated coupon sales, and overstated revenue and expenses. Luckin’s share price increased 100% from the IPO price.[27]

Equity offering and bond issuance in January 2020: Luckin obtained an equity offering and convertible bond offering of about USD418 million and USD446.7 million, respectively. These offerings were based on the fabricated financial performance as mentioned above. Within eight months of Luckin’s IPO listing, the company’s stock price increased 200%.[28]

The Accounting Scandal and Fraud at Luckin Coffee

Luckin made false statements and fabricated its financial performance to lure in investors. Luckin failed to disclose accurate revenue and expenses, and also obtained money through false bank statements. Moreover, Luckin failed to maintain adequate internal accounting controls or keep accurate financial records. The company knew its financial statement and records were misleading and deceptive. Luckin conspired with funding companies, vendors, and third-party shell companies to fabricate expenses and costs.

OUTCOME

The US Securities and Exchange Commission, the Chinese securities regulator, and China’s State Administration for Market Regulation, opened an investigation into Luckin’s conduct. It was found by the US SEC that Luckin’s misconduct constituted fraud.

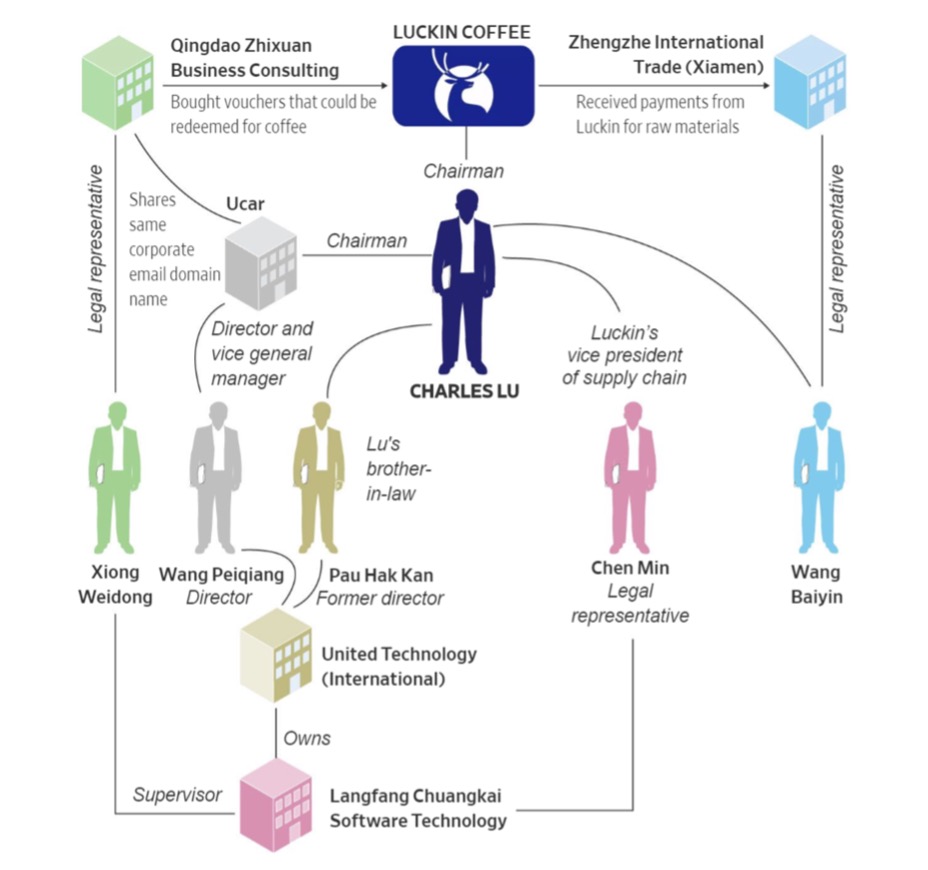

After which, on 2 April 2020, Luckin’s share sank 81%. Trade in Luckin shares was initially suspended, but it was resumed on 20 May 2020. Luckin also conducted an internal investigation and in April 2020 announced that more than USD300 million was fabricated in 2019, and the relevant public financial reports should be ignored. Twelve employees who worked with the CEO and COO involved in the three schemes were fired, and by July 2020, Luckin’s CEO, Jenny Zhiya Qian, was fired.[29] Furthermore, evidence showed the companies which purchased the coupons had links to the chairman (see Figure 3). The chairman was removed in July 2020.[30]

The SEC charged Luckin with fabricating untrue statements from April 2019 to January 2020 regarding revenue, expenses, and net loss so as to deceive investors about Luckin’s financial performance.[31] The SEC finalized the investigation and announced a penalty against Luckin on 16 December 2020. This resulted in Luckin agreeing to a settlement, including permanent injunctions and paying USD180 million in monetary penalties. Luckin has not admitted to or denied the allegations.[32]

ANALYSIS OF ETHICAL ISSUES

Luckin’s ethical failure was the management intentionally misrepresented the company and produced false accounting documents to mislead investors for their own advantage. Ethics analysis in this case includes all levels of a company, including senior management, the board of directors, audit committee, internal auditors, and external auditors, while discussions are related to conflicts of interest, dishonesty, abusing positions of power, and failure to fulfil fiduciary duties.

Fraud is usually due to multiple parties’ misconduct, including senior management, frontline staff, internal auditors, and external auditors. However, management has the duty to ensure the maintenance of ethical standards in a company. In Luckin’s case, several moral agents failed to fulfil their moral responsibilities, which led to the accounting scandal and fraud.

Three core elements led to fraud in Luckin’s case: (1) internal pressure to reach unrealistic sales targets through coupon sales and redemption, (2) reckless company management creating the opportunity for fraud, and (3) rationalising it was acceptable to fabricate financial statements to meet targets.

Responsibility for Ethical Failures

1. Lack of Integrity and Commutative Justice

Luckin’s Senior Management

Senior managers lacked the incentive to maintain their ethics and fiduciary duties with non-investors, including employees and vendors. There is evidence showing the chairman instructed his employee to fabricate transactions.[33]Further, management set unrealistic targets for short-term sales performance, creating unnecessary pressure on employees and preventing the company’s long-term success.

Integrity is an essential element of financial ethics and its lack affects the trust between investors and senior management. Investors expect management to behave honestly, which includes full and transparent disclosure of financial statements. However, the senior management in Luckin’s case intentionally encouraged false accounting to deceive auditors and prepared false financial statements to mislead investors. In addition, investors expected that Luckin would provide full and accurate public financial statements, which the company failed to do.

Commutative justice is a form of justice relevant in finance and business transactions. Commutative justice relates to fairness in the exchange of goods or services. In other words, justice in a market exchange related to a contractual relationship based on integrity, fairness, and accuracy. To fulfil a contractual obligation, the seller has the responsibility to disclose information thoroughly and accurately. The seller and buyer negotiate the market price based on the information consistent with the actual value of the goods or services. In Luckin’s case, the share price increased because of overstated revenue and expenses. Thus, the company deceived investors and violated commutative justice.

2. Failure to spot unethical practices

Luckin’s Board of Directors

Luckin’s directors failed to monitor, supervise management, and establish an ethical culture. There is doubt regarding whether the directors questioned Luckin’s aggressive plan or its rapid growth in the market share of coffee in China. Luckin’s directors failed to ask any questions or spot the unethical practices. Though Muddy Waters Research released its report in February 2020, the directors kept silent and did not raise any red flags as they should have. This could be a result of prioritizing short-term profits and overlooking behavioural pitfalls. Board culture such as dominant leadership, groupthink, and confirmation bias can increase the chance of accounting scandals.[34] A more effective code of ethics can encourage directors to identify bad conduct earlier and mitigate the risk of fraud. It is therefore necessary to establish a strong sense of honesty and openness throughout the company, from the directors to the frontline staff, so staff feel secure enough to report any misconduct.

3. Violating Code of Ethics

Audit Committee

An audit committee has a duty to apply the code of ethics and ensure the company acts honestly and not be swayed by the share price and its relationship with management. However, in this case, the audit committee kept silent and failed to notify the board of potential ethics infringement.

Internal Auditors

Integrity, objectivity, and competency are the core elements of the code of ethics among internal auditors. Internal auditors are the first defensive line in the prevention of financial misstatement. Internal auditors need to be trustworthy, as trust is fundamental to their profession. Furthermore, without being influenced by a third-party or their interests, internal auditors must have high standards of objectivity when collecting and evaluating information and making balanced judgements. They should apply their knowledge, skills, and experience to ensure the accuracy of the system. However, Luckin’s internal auditors cooperated with the fabricated transactions and violated their code of ethics.

4. Conflicts of Interest

External Auditor

EY wrote a private letter to a number of investment banks stating it did not have an issue with the financial performance of Luckin in the first three quarters of 2019.[35] This letter was issued before the 2019 financial statements were audited. EY’s letter raised a few questions. First, EY’s letter might represent a guarantee there was no problem with Luckin’s finances. However, the purpose of due diligence is to express the auditor’s opinion of reasonable assurance. It is not a guarantee that financial performance is free of error.[36] It might appear the EY letter was deceiving the investment banks into believing there was no issue with Luckin. Although EY did not audit Luckin’s 2019 financial statement, EY is not necessarily absolved of responsibility.

According to EY’s two statements, the auditor stated it identified the inflated financial results and reported it to the board.[37] They also raised red flags regarding Luckin’s misstatement in early 2020. It is therefore likely that EY noticed the fabricated statement and discovered the fraud. EY chose to quietly withdraw as an auditor from the client, possibly due to a conflict of interest between the firm and its own investors, and did not report the potential fraud to regulators. A conflict of interest is something which “jeopardizes an individual’s ability to act ethically by interfering with his or her capacity to exercise good judgment. This interference may lead to wilful neglect of the individual’s professional or public obligation”.[38] An auditor has an obligation to reasonable assure the accuracy of the financial performance of its client. As a commercial firm, EY’s revenue depends on its relationships with its clients, which may create a conflict of interest – the client’s interests override public interest. EY failed to act ethically by not reporting the potential fraud to the regulators, and instead serving the interests of the client. Instead, EY issued a letter to the investment banks, stating that Luckin had no financial irregularities. As a professional accounting firm, EY has a responsibility to consider public interest and a duty of transparency and integrity. To avoid structural conflict of interest and improve regulatory oversight, separating audit practices from other business units might encourage auditors to act independently.

Conclusion

Several parties are responsible for the accounting scandal and fraud at Luckin. Luckin should have established and applied a more robust code of ethics throughout the company, from senior management to frontline staff, in order to detect fraud at an earlier stage and to remain consistent with commutative justice. External auditors should have been more proactive in raising red flags regarding the company’s misconduct, as well as avoided guaranteeing financial performance to other parties until the firm had conducted its due diligence. Regulatory agencies also play a role in preventing improper transactions by implementing and enforcing laws. There are monitoring, investigation, and moral obligations between regulators and publicly listed companies. The regulators in China and the US should have ensured that Luckin fulfilled its duty of integrity and transparency before listing. A more comprehensive and rigorous system may have brought Luckin’s fraud to light earlier.

Looking ahead, structural changes could reduce the risk of fraud. First, increasing regulators’ powers of enforcement could expedite the investigation process and minimise the negative impact of fraud. Second, providing more fraud detection training for auditors would increase their skills and ability to spot improper transactions. Third, increasing transparency and stringent vetting of the internal auditing system would help auditors make balanced judgements from all perspectives. Finally, as historian A. J. P. Taylor once said, “Nothing is inevitable until it happens”. Hopefully, the Luckin case raises awareness about the importance of multilevel cooperation on a company’s financial ethics and moral culture.

[1] Luckin Coffee, Press Release and Statements, “Luckin Coffee announces smart unmanned retail strategy, bringing Luckin closer to customers” 7 January 2020 < https://investor.luckincoffee.com/news-releases/news-release-details/luckin-coffee-announces-smart-unmanned-retail-strategy-bringing>.

[2] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020.

[3] Ibid.

[4] US Securities and Exchange Commission, “Luckin Coffee Agrees to Pay $180 Million Penalty to Settle Accounting Fraud Charges”, 2020-319, 16 December 2020, Press Release < https://www.sec.gov/news/press-release/2020-319>

[5] Winky T. Yang, “Profit and Ethics in Short Selling: The Case of Muddy Waters”, 6 January 2015 < https://sevenpillarsinstitute.org/profit-ethics-short-selling-case-muddy-waters/>

[6] Ben Coley, “Luckin Coffee Faces Fraud Allegations from Anonymous Report”, QSR, January 2020 < https://www.qsrmagazine.com/fast-food/luckin-coffee-faces-fraud-allegations-anonymous-report>.

[7] Ben Coley, “Luckin Coffee Faces Fraud Allegations from Anonymous Report” January 2020 < https://www.qsrmagazine.com/fast-food/luckin-coffee-faces-fraud-allegations-anonymous-report>

[8] Anonymous Report, “Luckin Coffee: Fraud + Fundamentally Broken Business”, 2020 <https://drive.google.com/file/d/1LKOYMpXVo1ssbWQx8j4G3-strg6mpQ7F/view>.

[9] Anonymous Report, “Luckin Coffee: Fraud + Fundamentally Broken Business”, 2020 <https://drive.google.com/file/d/1LKOYMpXVo1ssbWQx8j4G3-strg6mpQ7F/view>.

[10] Saqib Iqbal Ahmed, “Luckin Coffee share price may nearly double to $60 on US exchanges: hedge fund Citron Capital, Reuters, 5 February 2020 < https://www.reuters.com/article/us-luckin-coffee-stock-citron-idUSKBN1ZY2EK>

[11] 33,000,000 Amercian Depositary Shares, Luckin Coffee Inc. “Representing 264,000,000 Class A Ordinary Shares <https://investor.luckincoffee.com/node/6391/html>

[12] GlobeNewswire, “Luckin Coffee Received Notification from Mr. Tianruo Pu of his resignation as an Independent Director”, 19 June 2020 < https://www.globenewswire.com/news-release/2020/06/19/2050625/0/en/Luckin-Coffee-Received-Notification-from-Mr-Tianruo-Pu-of-his-Resignation-as-an-Independent-Director.html>.

[13] Russell Flannery, “Responsibility for Luckin Coffee’s Accounting Debacle Is Far And Wide”, 3 April 2020, <https://www.forbes.com/sites/russellflannery/2020/04/03/responsibility-for-luckin-coffees-accounting-debacle-is-far-and-wide/?sh=a7be566104e4>

[14] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020, Paragraph 29-30.

[15] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020, Paragraph 30.

[16] Jing Yang, “Ernst & Young Says It Isn’t Responsible for Luckin Coffee’s Accounting Miscouduct”, Wall Street Journal, 17 July 2020 <http://www.chinabevnews.com/2020/07/ernst-young-says-it-isnt-responsible.html>.

[17] Ibid.

[18] Nasdaq, “Luckin Coffee Inc. (LK)” < https://www.nasdaq.com/market-activity/ipos/overview?dealId=1083391-89499>

[19] Yang Ge, Shen Xinyue, Wei yiyang and Qu Yunxu, “Luckin Explained: How Did Scandal-Plagued Coffee Highflyer Get Into Such Hot Water?” 20 May 2020, Caixin < https://www.caixinglobal.com/2020-05-20/luckin-explained-how-did-scandal-plagued-coffee-highflyer-get-into-such-hot-water-101556560.html>

[20] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020, Paragraphs 21- 30.

[21] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020.

[22] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020, Paragraphs 21- 22.

[23] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020, Paragraph 28.

[24] Jian Yang, “Behind the Fall of China’s Luckin Coffee: a Network of Fake Buyers and a Fictitious Employee”, 28 May 2020 < https://www.wsj.com/articles/behind-the-fall-of-chinas-luckin-coffee-a-network-of-fake-buyers-and-a-fictitious-employee-11590682336>.

[25] Case Securities and Exchange Commission vs Luckin Coffee, Inc., 1:20-cv-10631, United States District Court Southern District of New York, 16 December 2020.

[26] Ibid.

[27] Ibid.

[28] Ibid.

[29] Luckin Coffee, “Luckin Announces the Substantial Completion of the Internal Investigation”, 1 July 2020 < https://investor.luckincoffee.com/news-releases/news-release-details/luckin-announces-substantial-completion-internal-investigation>

[30] Ben Coley, “Luckin Coffee Agrees to Pay $180 Million Fine for Fraud Scandal”, QSR, 17 December 2020 <https://www.qsrmagazine.com/finance/luckin-coffee-agrees-pay-180-million-fine-fraud-scandal>.

[31] US Securities and Exchange Commission, “Luckin Coffee Agrees to Pay $180 Million Penalty to Settle Accounting Fraud Charges”, 2020-319, 16 December 2020, Press Release < https://www.sec.gov/news/press-release/2020-319>

[32] Ibid.

[33] Anna Vod, “Chariman of Luckin Coffee Allegedly Fraud” CapitalWatch, 9 Jun 2020 < https://www.capitalwatch.com/article-5769-1.html>.

[34] Mak Yuen Teen, “What the Wirecard and Luckin Coffee scandals can teach Asia’s boards”, Nikkei Asia, 21 August 2020 <https://asia.nikkei.com/Opinion/What-the-Wirecard-and-Luckin-Coffee-scandals-can-teach-Asia-s-boards>.

[35] Ibid.

[36] Drew Bernstein, “Who is responsible for preventing frauds?” In Forensic Accounting, MBP, < https://crm.marcumbp.com/china-accounting-insights/who-is-responsible-for-preventing-frauds>.

[37] Jing Yang, “Ernst & Young Says It Isn’t Responsible for Luckin Coffee’s Accounting Misconduct” 17 July 2020 < http://www.chinabevnews.com/2020/07/ernst-young-says-it-isnt-responsible.html>

[38]Seven Pillars Institute, “Conflict of Interest” 26 August 2017 < https://sevenpillarsinstitute.org/glossary/conflict-of-interest/>